Message: Return type of CI_Session_null_driver::open($save_path, $name) should either be compatible with SessionHandlerInterface::open(string $path, string $name): bool, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_null_driver::close() should either be compatible with SessionHandlerInterface::close(): bool, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_null_driver::read($session_id) should either be compatible with SessionHandlerInterface::read(string $id): string|false, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_null_driver::write($session_id, $session_data) should either be compatible with SessionHandlerInterface::write(string $id, string $data): bool, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_null_driver::destroy($session_id) should either be compatible with SessionHandlerInterface::destroy(string $id): bool, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_null_driver::gc($maxlifetime) should either be compatible with SessionHandlerInterface::gc(int $max_lifetime): int|false, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

NRIPage | Articles | Fixed vs Floating Home Loan Interest Rates: Which One Should You Choose | Get Nutrition Food & Beverages. Get food tips, trends and create memorable nutritious dining experiences - NRI Page

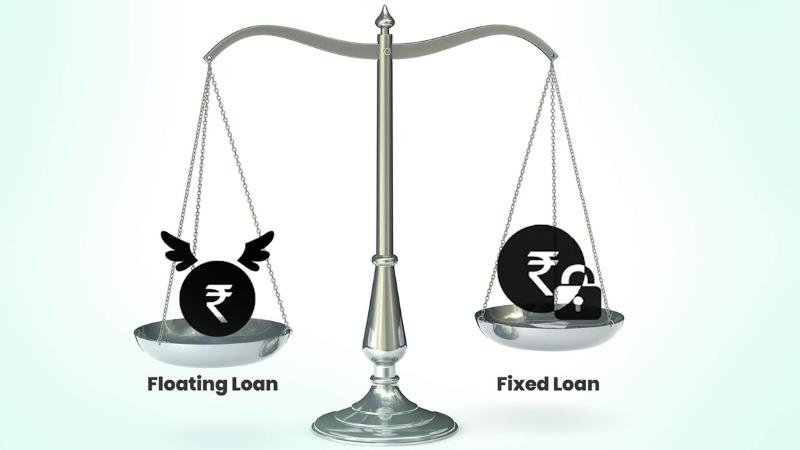

Choosing between a fixed and floating interest rate for a home loan is a crucial financial decision. Both options come with advantages and risks, and selecting the best one depends on your financial goals, market trends, and risk appetite. A fixed rate offers stability, while a floating rate provides flexibility and potential savings. Understanding the differences between these loan types will help you make an informed decision based on your repayment capacity and future market expectations.

Fixed Interest Rates: Stability but Higher Costs

A fixed interest rate means your Equated Monthly Installments (EMIs) remain constant throughout the loan tenure. This option is ideal for borrowers who prefer financial security and want to avoid market fluctuations.

Predictability: Fixed EMIs make budgeting easier since the repayment amount does not change.

Protection from rate hikes: Even if market interest rates increase, your loan remains unaffected.

Best for short tenures: Fixed rates are more suitable for loans with 3 to 10-year tenures, ensuring stability.

However, there are some downsides:

Higher interest rates: Fixed rates are 1% to 2.5% higher than floating rates.

No benefit from rate cuts: Even if market rates decrease, you will continue paying the higher fixed rate.

Floating Interest Rates: Lower Costs but Market-Dependent

A floating interest rate varies with market conditions. This means your EMI can increase or decrease based on financial trends. Floating rates are usually lower than fixed rates, making them an attractive option when rates are expected to remain stable or decline.

Lower interest rates: Floating rates are usually cheaper than fixed rates, helping borrowers save money.

Reduced EMI when rates drop: If the market interest rate decreases, your loan repayment burden decreases.

No prepayment penalty: Borrowers can repay the loan early without additional costs, unlike fixed-rate loans.

However, floating rates come with uncertainty:

EMIs fluctuate: If interest rates rise, your monthly payment increases, affecting your budget.

Not ideal for short-term loans: The savings benefit is more noticeable in long-term loans of 20 to 30 years.

Which One Should You Choose?

Choose a fixed interest rate if you prefer stability and predictable EMIs or if market rates are expected to rise.

Choose a floating interest rate if you expect interest rates to decline or are comfortable with market fluctuations.

Short-term loans (3-10 years) are generally better with fixed rates, while long-term loans (20-30 years) can be cheaper with floating rates.

Ultimately, the best home loan interest rate depends on your financial goals, risk tolerance, and repayment strategy. Evaluating market conditions and your income stability will help you make the right choice.